Risk and Uncertainty in Insurance

Table of Contents

ToggleRisk and uncertainty are fundamental concepts that underpin the entire insurance industry. At its core, insurance is designed to mitigate the financial impact of risk and uncertainty, providing individuals and businesses with protection against unforeseen events that could cause significant loss. Risk refers to situations where the probability of an event occurring is known, while uncertainty arises when the likelihood of an event is unknown or cannot be predicted with precision. In the context of insurance, the management of both risk and uncertainty is critical to ensuring that insurers can offer coverage while maintaining financial stability.

The insurance industry operates by pooling the risks of many individuals or entities, spreading potential losses across a large group to reduce the financial burden on any single participant. Through the process of underwriting, insurers assess and categorize risks, assigning appropriate premiums based on the likelihood and severity of loss. However, uncertainty remains an inherent part of the process, as not all risks can be accurately predicted or quantified. The interplay between risk and uncertainty shapes the development of insurance products, pricing strategies, and claims handling, making it essential for insurers to constantly adapt to changing circumstances.

This article explores the concepts of risk and uncertainty in insurance, their implications for both insurers and policyholders, and the strategies employed by the insurance industry to manage these challenges. By understanding how risk and uncertainty influence insurance practices, we can better appreciate the vital role insurance plays in mitigating the potential financial impact of unpredictable events.

Risk in Insurance

Risk refers to situations where the probability of different outcomes is known or can be estimated. In insurance, risk involves events that might lead to a financial loss, but the likelihood of these events occurring can be calculated based on past experiences, data, and statistical methods.

Pure Risk

Pure risk is the type of risk that insurance companies typically deal with, as it involves only the possibility of loss or no loss, and no possibility of gain. In contrast to speculative risks, which can result in either gains or losses (such as stock market investments), pure risks are unidirectional in nature.

Examples of pure risk include:

- Death: Life insurance covers the risk of premature death.

- Illness: Health insurance provides coverage for unexpected health issues.

- Accidents: Auto insurance covers risks related to car accidents, injuries, or vehicle damage.

- Natural disasters: Property insurance can protect against the financial impact of floods, fires, or earthquakes.

The insurer’s role is to assess the probability of such events happening and to provide coverage against the financial consequences of these risks.

Speculative Risk

Speculative risk involves situations where there is a chance of both gain and loss. This type of risk is typically not insurable, as the outcome is uncertain in both directions, making it difficult for insurance companies to assess or price.

Examples of speculative risk include:

- Investments in the stock market or real estate.

- Business ventures, where a company might succeed or fail based on market conditions, competition, or innovation.

While speculative risks can lead to losses, they are not usually covered by insurance because they involve opportunities for profit or loss, making them outside the scope of traditional insurance.

Underwriting Risk

Underwriting risk refers to the risk that the insurer’s underwriting assumptions (such as the likelihood of claims) prove to be incorrect. Insurers rely on actuarial data and statistical models to assess the risk associated with insuring individuals or businesses. However, these models are based on assumptions that may not hold true in practice.

For example, if an insurer underestimates the frequency or severity of claims in a given pool of policyholders (e.g., based on past health trends or accident rates), they may face a higher-than-expected number of claims. This leads to higher payouts and can strain the insurer’s financial stability.

Moral Hazard

Moral hazard occurs when individuals or organizations change their behavior because they are insured. Knowing that they are covered against financial losses, they may take more risks or behave less cautiously than they would without insurance.

For example:

- A person with health insurance might neglect preventive care, assuming that any medical expenses will be covered by their insurer.

- A homeowner with comprehensive insurance may be less concerned about securing their property or preventing damage.

- Insurers work to mitigate moral hazard through policy design, such as by imposing deductibles or exclusions for certain behaviors (e.g., requiring the use of safety equipment for workers in certain industries).

Operational Risk

Operational risk refers to the internal risks that an insurance company faces due to failures in its systems, processes, or human factors. These risks can arise from a variety of issues, such as:

- Fraud: Employees or customers may engage in fraudulent activities that affect the insurer’s bottom line.

- System failures: A cyberattack or IT system outage can disrupt an insurer’s ability to process claims, issue policies, or assess risks.

- Human error: Mistakes made by insurance underwriters, claims adjusters, or other staff members can lead to financial losses or operational disruptions.

Insurance companies must invest in robust internal controls, cybersecurity, training, and risk management frameworks to minimize these operational risks.

Catastrophic Risk

Catastrophic risk involves the possibility of large-scale, unpredictable events that cause significant damage and result in extremely high claims. These risks are difficult to predict, but their potential impact on insurers is immense.

Examples include:

- Natural disasters such as hurricanes, earthquakes, and floods.

- Pandemics, such as COVID-19, that cause widespread health and economic disruption.

- Insurers typically manage catastrophic risks through the use of reinsurance (discussed below) or by setting aside large reserves to cover such events.

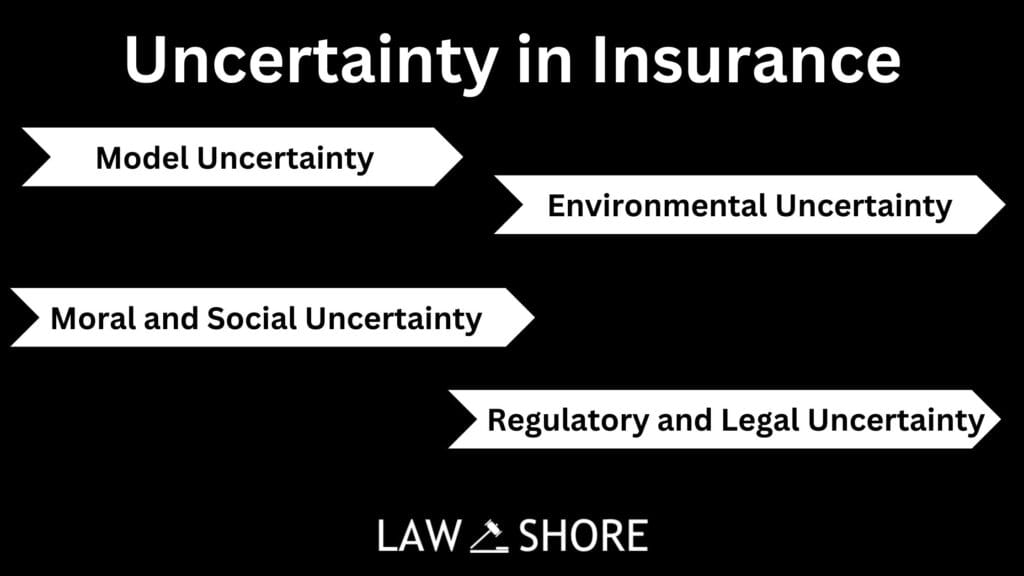

Uncertainty in Insurance

Uncertainty refers to situations where the probability of future events is unknown or cannot be predicted accurately. This stands in contrast to risk, where probabilities can be estimated. Uncertainty represents an inherent lack of knowledge about future outcomes that may influence both individuals and insurers.

Model Uncertainty

Model uncertainty arises because insurance companies rely heavily on statistical models and historical data to predict risk. However, these models are based on assumptions that might not hold true under future conditions.

- New Risks: For instance, emerging risks such as cyberattacks or climate change may not be fully captured by traditional models. The occurrence of an event like a cyberattack or the intensity of climate events may not follow historical trends.

- Changing Behavior: Human behaviour, technology, and other factors evolve, making it difficult to account for all future contingencies. For example, advancements in medical treatment or shifts in consumer behavior could alter health insurance claims in ways that models can’t foresee.

Environmental Uncertainty

Environmental uncertainty involves the unpredictability of external factors that influence insurance, such as:

- Climate change: The increasing frequency and severity of natural disasters like hurricanes, wildfires, and floods create unpredictable risks for insurers.

- Political instability: Changes in political or economic conditions—such as a country’s financial crisis or regulatory shifts—can disrupt insurance markets.

- Technological disruptions: Rapid technological advances (e.g., autonomous vehicles or AI) could change the risk landscape for auto or liability insurance, making past data less relevant.

Insurers struggle to predict how these uncertainties will manifest, and they often adjust their pricing models and reserve strategies to account for such environmental volatility.

Moral and Social Uncertainty

Moral and social uncertainty refers to unpredictable shifts in societal attitudes, values, or ethical norms that can impact insurance.

- Changes in social norms: For example, increasing awareness of mental health or lifestyle diseases may affect how health insurers price policies or what coverage they provide.

- Legal and regulatory changes: New laws or regulations (such as those related to climate risk disclosure, social justice concerns, or data privacy) may lead to unforeseen liabilities or operational challenges for insurers.

This kind of uncertainty can make it difficult for insurers to set long-term strategies or predict future claims based on the evolving nature of society.

Regulatory and Legal Uncertainty

The regulatory landscape for insurance can change, creating legal uncertainty for both insurers and policyholders. Governments may introduce new regulations (e.g., insurance solvency rules, data protection laws, or mandates for coverage) that alter the business environment.

- Uncertainty from new regulations: For example, in the European Union, the introduction of the Solvency II directive set stricter capital requirements for insurers, impacting their risk-taking behavior.

- Litigation risk: A shift in legal environments can lead to an increase in the frequency or size of claims. For example, a ruling that expands liability for certain damages (e.g., product liability or environmental contamination) could create unexpected exposures for insurers.

Managing Risk and Uncertainty in Insurance:

- Diversification:

Diversification is a key strategy used by insurers to manage risk. By spreading their exposure across multiple lines of business, geographical areas, and customer types, insurers reduce the impact of any single event or loss. For example:

-A health insurer may offer policies across different regions, reducing the risk of a localized health crisis.

-An insurance company offering both auto and home insurance can offset losses from a catastrophic natural disaster by drawing on more predictable lines of business. - Reinsurance:

Reinsurance is insurance for insurers. When an insurer faces a large amount of risk, it can transfer some of that risk to a reinsurance company, thus limiting its exposure to catastrophic losses. This helps stabilize the insurer’s finances and ensures that it can meet obligations in the event of major claims.

For example, a property insurer facing the risk of huge losses due to a major earthquake might purchase reinsurance to cover a portion of the claims. The reinsurer would take on a portion of the risk for a premium, allowing the primary insurer to avoid catastrophic losses. - Statistical Modeling and Actuarial Science:

Insurance companies use statistical modelling and actuarial science to predict the likelihood of various events and set prices for premiums accordingly. Actuaries use historical data to estimate the probability of an event occurring and the potential cost, helping insurers maintain financial solvency. These models are regularly updated to reflect new data, helping to adjust pricing and coverage for emerging risks. - Risk Pooling:

Risk pooling is the process of combining risks from a large number of policyholders. By aggregating the risks of many individuals or organizations, insurers can reduce the financial impact of a single event. The more diversified the pool, the more predictable the overall claims experience becomes, even if individual claims remain uncertain. - Risk Mitigation and Loss Prevention:

Many insurers offer loss prevention strategies or incentives to policyholders to reduce the likelihood of claims. For example:

– Homeowners might get discounts for installing fire alarms, smoke detectors, or security systems.

-Health insurers might offer discounts for regular checkups or gym memberships to encourage healthier lifestyles. These preventive measures help reduce overall risk and claim frequency. - Contingency Planning:

Insurers maintain contingency reserves and engage in scenario planning to handle uncertainty. They estimate the worst-case scenarios (such as major natural disasters or financial crises) and plan for how they would manage such situations, both financially and operationally. This includes maintaining solvency through adequate capital reserves and contingency plans for disruptions. - Pricing Strategy:

Insurers set premiums based on their estimates of risk and uncertainty. They adjust premiums in response to changing conditions or unexpected losses. For example, if the frequency of natural disasters increases, the insurer may raise premiums for policyholders in affected areas or add new clauses to exclude certain risks.

Key Takeaways:

- Risk involves measurable probabilities of loss, while uncertainty represents unknown or unpredictable events.

- Insurance companies use various tools like diversification, reinsurance, statistical models, and loss prevention to manage risk and cope with uncertainty.

While risk can often be quantified and mitigated, uncertainty requires adaptability and contingency planning, making it a constant challenge for the insurance industry. - In essence, the insurance business is about managing the balance between the known (risk) and the unknown (uncertainty), while constantly evolving to handle emerging challenges.

Conclusion

Risk and uncertainty are inextricable elements of the insurance industry, shaping both the design and pricing of insurance products. While risk is quantifiable and manageable to a certain extent through underwriting and actuarial analysis, uncertainty remains a persistent challenge that requires insurers to continuously adapt their strategies and models. Insurance, at its core, is a mechanism for sharing the burden of financial loss arising from risks that cannot be avoided or predicted with certainty. Through diversification, pooling of risks, and the application of sound risk management practices, insurers can provide a sense of security to individuals and businesses alike, even in the face of unforeseen events.

However, the dynamic nature of risk and the unpredictable nature of uncertainty necessitate that the insurance industry remain agile. Advances in technology, data analytics, and risk modelling are helping insurers better assess and manage both known risks and emerging uncertainties. As new risks, such as those associated with climate change, cyber threats, and global pandemics, continue to emerge, the role of insurance as a tool for risk mitigation will only become more critical.

Ultimately, while insurance can never eliminate risk or uncertainty, it serves as a vital financial safeguard, helping individuals and organizations navigate an increasingly unpredictable world. By understanding the relationship between risk and uncertainty, both insurers and policyholders can make more informed decisions, fostering a system that balances protection with sustainability.

Explore Law Shore: law notes today and take the first step toward mastering the fundamentals of law with ease.

After Completing my LLB hons, I started writing content about legal concepts and case laws while practicing. I finally started Law Shore in 2024 with an aim to help other students and lawyers.